Applying for a June 2026 BTO? Get the application and the financing right before you submit

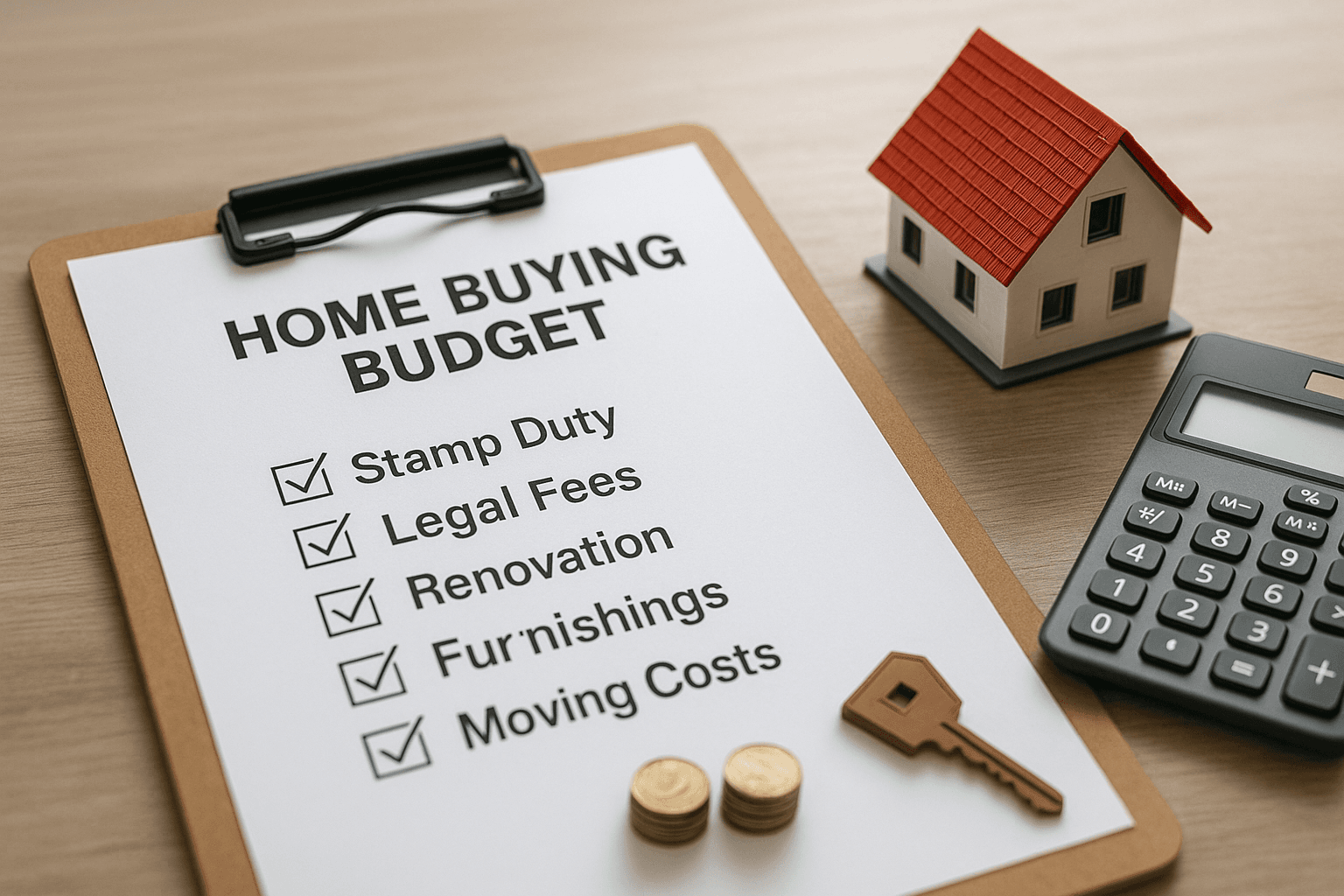

The June 2026 BTO launch covers projects in Ang Mo Kio, Bishan, Berlayar, and Sembawang North, with applications closing within days of launch. Before submitting, buyers should calculate the actual monthly cash gap beyond CPF contributions, understand MSR, TDSR, and LTV limits, and choose a project whose financing is genuinely manageable. If you spot an error after submitting, email HDB directly before cancelling, as corrections can be made without forfeiting your deposit or reapplying.

Sarah Chen·23 Jun 2026

Sarah Chen·23 Jun 2026