Singapore home buyers have a simple choice: take an** HDB loan** (fixed at 2.6%) or a bank loan, available with floating and fixed rate.

The HDB rate has been unchanged at 2.6% since 1999, set 0.1 percentage points above the CPF Ordinary Account (OA) interest rate of 2.5%. Bank loans, by contrast, move with market rates — usually 3-month compounded SORA + a spread.

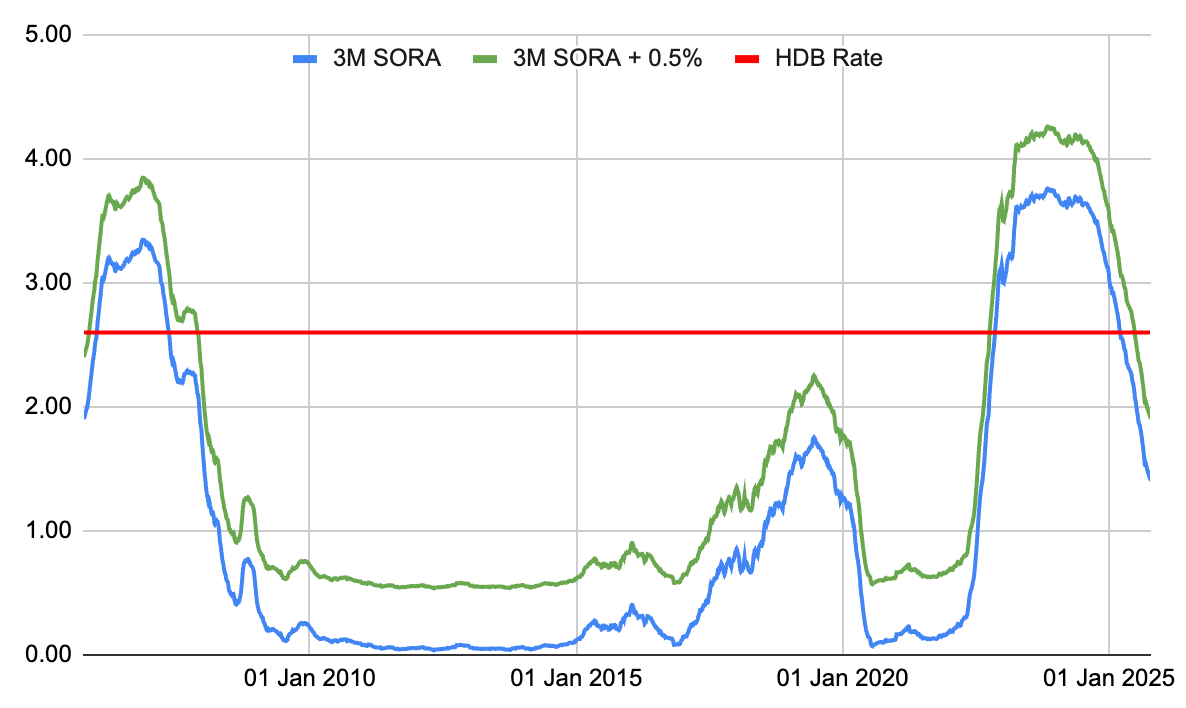

With 20 years of SORA data now available (since its introduction in 2005), we can finally compare how both options have really performed.

The chart below tells the story clearly.

The red line shows the constant 2.6% HDB rate.

The green line tracks the 3-month compounded SORA + 0.5%, the realistic cost of a typical floating bank loan.

The blue line is the raw 3-month SORA itself.

Source: 3-months compounded SORA by MAS

Across the full 20-year period (2005 – 2025):

Bank loans were cheaper than HDB loans for 182 out of 240 months.

Only two periods saw bank rates exceed 2.6% — from 2005 to 2007, and again 2023 to 2024 during the global rate spike.

That means roughly 76% of the time, borrowers with bank loans enjoyed lower interest rates.

Let’s put that in concrete terms.

If you borrowed S$500,000 in 2005 for 20 years, here’s what would have happened:

| Loan Type | Average Rate | Total Repaid (20 yrs) | Interest Paid | Difference |

|---|---|---|---|---|

| HDB Loan | Constant 2.6% | ≈ S$642,000 | ≈ S$142,000 | – |

| Bank Loan (3M SORA + 0.5%) | Variable (typically 1–2.5%) | ≈ S$572,000 | ≈ S$72,000 | ≈ S$70,000 less |

So while both loans have their merits, bank borrowers paid about S$70,000 less in total interest over the same 20-year period.

Even if you had chosen a fixed-rate bank loan instead of a floating one, the overall outcome would have been very similar. That’s because fixed-rate packages in Singapore are ultimately priced off the same SORA benchmark — the bank simply “locks in” a rate (for example, 2.00%, representing SORA plus a spread) for a limited period.

In other words, fixed-rate loans don’t operate in a different universe — they’re just temporary shields against short-term rate movements. Over a 20-year tenure, a borrower will typically refinance several times, so the long-term cost difference between fixed and floating packages is usually minimal. The main advantage of a fixed rate is short-term stability, not necessarily a lower total cost.

HDB loans offer unbeatable convenience, especially for first-time BTO buyers:

No cash downpayment (you can use CPF fully)

Lower upfront income and credit requirements

That’s why it’s smart to start with an HDB loan when buying your first BTO flat.

It lets you secure your home safely while construction completes — often over 3–5 years.

Once you’ve collected your keys, your loan formally begins, and that’s the perfect time to refinance to a bank loan.

Here’s why:

Lower interest rate potential: Banks typically price at SORA + 0.5–0.8%, which historically stays below 2.6%.

Flexible packages: You can choose fixed, floating, or hybrid structures to match your financial comfort.

Refinancing promotions: Banks often offer legal subsidies or cash rebates to attract refinancers.

Compounding savings: Even a 0.5% difference on a 20-year loan can mean tens of thousands saved.

In short, HDB loans are a good starting point, but bank loans win the long game.

Over the last 20 years, a borrower with a bank loan tied to 3-month SORA + 0.5% would have saved around S$70,000 versus staying with an HDB loan at 2.6%.

While past performance isn’t a guarantee of future rates, the data shows that refinancing after key collection can be one of the most impactful financial decisions a homeowner makes.

© 2026 Cashew. All rights reserved.