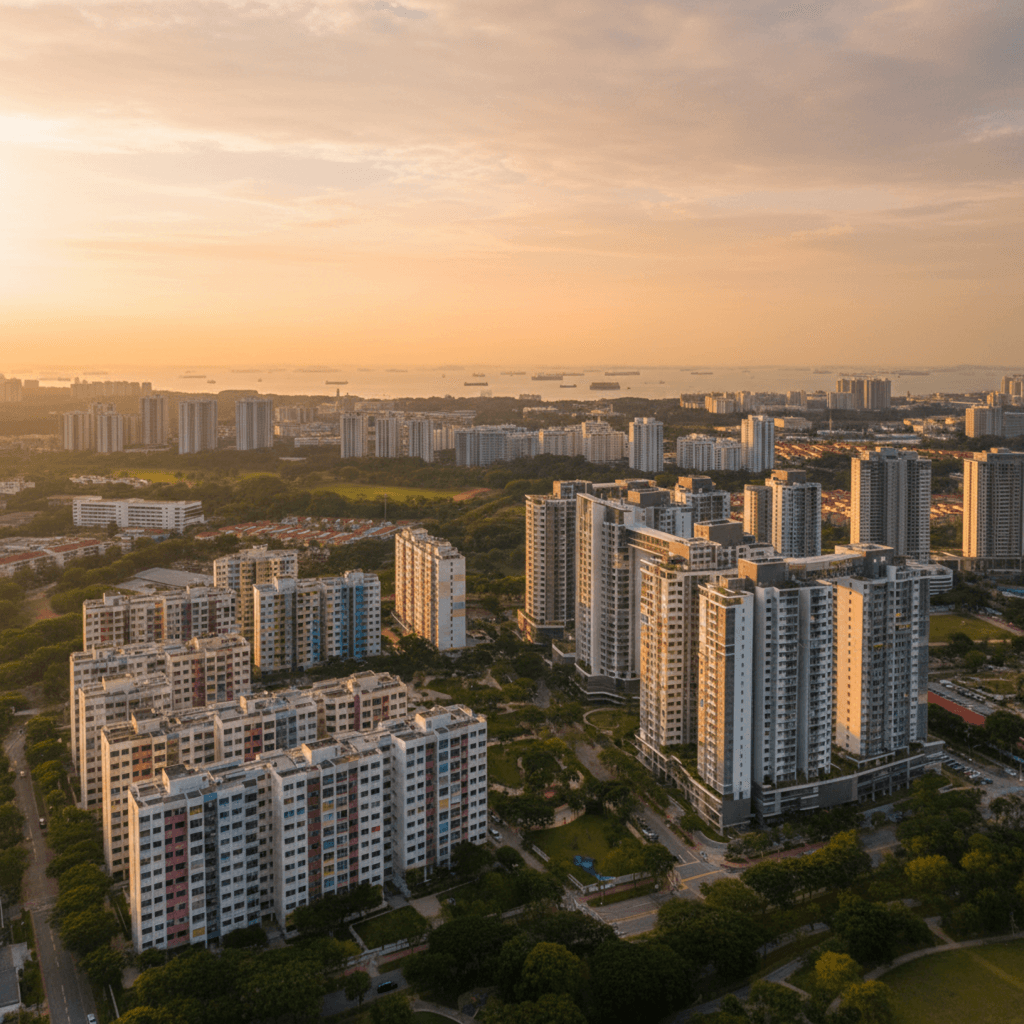

Liu Thai Ker, the architect who designed Singapore's iconic public housing system, died in January 2026 at age 87, leaving behind a legacy that housed 3 out of 4 Singaporeans. But his passing has reignited debate over whether the HDB model—celebrated globally for decades—is still sustainable as resale prices soar, million-dollar flats multiply, and 99-year leases tick closer to expiry.

For homebuyers and current HDB owners, these structural challenges intersect with a rare mortgage opportunity: bank loan rates at 1.35%–1.70% and SORA bottoming in Q2 2026. The question is whether to lock in refinancing savings now, or wait as the HDB market recalibrates in 2026–2027.

HDB resale prices have surged since the Covid-19 pandemic, driven by construction delays that pushed waiting times from three years to six years for new BTOs. As frustrated buyers turned to the resale market, demand spiked—and so did prices.

In 2025 alone, 1,594 HDB flats sold for more than S$1 million, up from just 82 in 2020. That's a 1,846% increase in five years. While HDB resale prices are projected to grow another 3%–4% in 2026, analysts warn that affordability constraints are now acting as a "natural brake" on further escalation.

What this means for you:

If you're a resale buyer, expect continued high prices in mature estates, but more supply hitting the market in 2026 (13,500 flats reaching MOP, up 69% from 2025) could moderate growth.

If you're an HDB owner considering upgrading or refinancing, your property value may have peaked—making now a strategic time to refinance and lock in equity.

Singapore's oldest HDB flats are now entering their final three decades, and the approaching lease expiry is eroding their value. Properties with less than 60 years remaining become harder to sell, and flats with under 20 years left lose most of their market value.

Liu Thai Ker himself warned before his death that "leaseholders must respect that at the end of 99 years, the flat goes back to the government." Yet many Singaporeans have come to view HDB flats as retirement nest eggs and wealth-building assets—a perception that clashes with the reality of depreciation.

What this means for you:

If your HDB has more than 60 years left, refinancing now at 1.35%–1.60% can free up cash to invest elsewhere or upgrade before depreciation accelerates.

If your flat has less than 60 years, consider whether upgrading to a newer resale flat or BTO makes financial sense, especially with shorter waiting times (under 3 years) now available.

HDB announced in January 2026 that it will launch 19,600 BTO flats this year, including over 4,000 units with waiting times under three years. Some projects, like Tampines Bliss, will be ready in just 1 year 11 months—the fastest since 2018.

This increased supply should ease pressure on the resale market, but demand remains intense. The government projects 15,000 couples will be looking to buy in 2026, competing for 13,500 resale flats reaching MOP—a supply-demand imbalance that will keep prices elevated.

What this means for you:

BTO applicants: With shorter waiting times, you can now plan your mortgage earlier. Use 2026 to compare bank packages (1.35%–1.70%) and lock in rates before SORA rises.

Resale buyers: More MOP flats entering the market in 2026 may give you slightly more negotiating power, but don't expect dramatic price drops.

If you're currently on HDB's 2.60% concessionary loan, refinancing to a bank package at 1.35%–1.60% could save you significant money:

S$300,000 loan: Save ~S$2,160/year

S$500,000 loan: Save ~S$3,600/year

S$700,000 loan: Save ~S$5,100/year

With SORA projected to bottom around 1.0%–1.2% in Q2 2026 before climbing to 1.39% by year-end, February–April 2026 is your optimal refinancing window.

Now–February: Compare packages on Cashew.sg, verify your TDSR eligibility at 4% stress test

February–March: Lock in your interest rate before SORA rises

April 2026: Complete refinancing before rates climb

Monitor resale trends: If your flat has appreciated significantly, consider whether refinancing frees up equity for upgrading

The FT article notes that HDBs remain far more affordable than private housing—HDB flats cost 4.3 times the median salary, while private homes cost 16.9 times. But for upgraders, the gap creates a significant financial hurdle, especially with ABSD at 17% for citizens buying a second property.

If you're planning to upgrade from HDB to private property in 2026, calculate your total upfront costs carefully:

25% down payment (5% cash + 20% CPF)

17% ABSD on the property price (S$255,000 on a S$1.5M condo)

BSD, legal fees, agent fees

Mortgage tip: Banks stress-test your TDSR at 4% minimum, not your actual loan rate. Make sure you can afford the monthly payments at 4% before committing.

Singapore's HDB model—designed by Liu Thai Ker to provide affordable housing and build national identity—is now facing challenges he anticipated but couldn't fully solve. Rising resale prices, the 99-year lease depreciation problem, and shifting demographics are testing the system's limits.

For homebuyers and HDB owners, 2026 presents both challenges and opportunities. Resale prices remain high but supply is increasing. BTO waiting times are shrinking. And most importantly, mortgage rates are at historic lows—creating a rare refinancing window before SORA climbs.

If you're on HDB's 2.60% loan, refinancing now could save you S$3,600–S$14,400+ annually. If you're planning to upgrade, lock in your financing before Q2 ends and rates rise.

Ready to explore your refinancing options? Cashew compares 500+ mortgage packages from all major Singapore banks—independent, transparent, and built to help you save. Start comparing today at Cashew.sg.

Sales proceeds are what remains after deducting your outstanding home loan, CPF refunds (principal plus accrued interest back to your own account), and selling costs such as agent commission and legal fees from your selling price. The CPF refund is the most commonly overlooked deduction, as accrued interest grows over time and the amount returned goes to your CPF account rather than as cash in hand. Understanding these deductions in advance helps you accurately plan for your next property purchase or financial move.

Chiltern Park's two-bedders achieved a 43.92% average ROI over a decade due to four identifiable factors: a low entry price relative to fair value, location scarcity limiting new supply, a unit size with broad buyer appeal, and a modest quantum that supports liquidity. Buyers can apply this same framework to any project by assessing entry price against district comparables, surrounding land availability, unit size demand depth, and loan affordability across a full rate cycle.

© 2026 Cashew. All rights reserved.