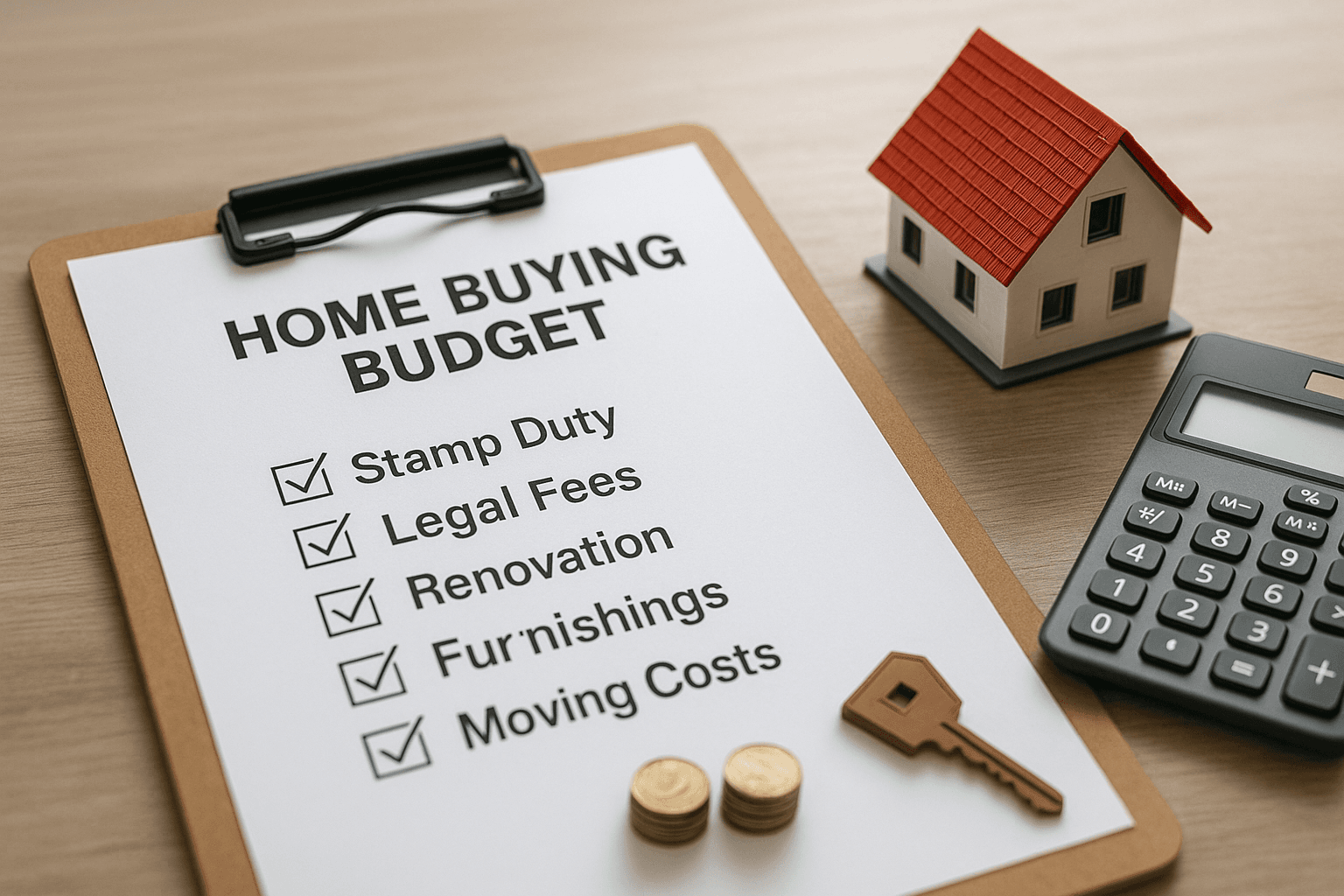

One of the biggest additional costs is Buyer’s Stamp Duty (BSD) – essentially a tax on acquiring property. In Singapore, BSD is calculated on the purchase price or market value (whichever is higher) on a sliding scale. For example, a $500,000 property might incur roughly $9,600 in BSD, while a $1,000,000 property would incur about $24,600 (rates increase with price tiers). If you’re a Singapore Citizen buying your first residential property, that’s the only stamp duty you pay. However, if you’re a Permanent Resident or foreigner, or if it’s your second property, Additional Buyer’s Stamp Duty (ABSD) may apply, which can be very hefty (PRs pay 5% on first property, citizens 0% on first but 20% on second as of recent rules, and higher for foreigners). First-timers usually avoid ABSD, but be aware of it if you plan to co-own with someone who already owns a home, etc. Stamp duties are payable within weeks of signing the purchase agreement – for private property, you must pay BSD (and any ABSD) within 14 days of exercising the Option to Purchase. For HDB, you’ll pay BSD around the completion appointment. Plan to have cash or CPF ready for BSD: for HDB purchases you can use CPF OA to cover BSD, but for private property BSD and ABSD, you typically need to pay in cash (or CPF if you have set it aside beforehand and arranged with your lawyer). Aside from stamp duty, there’s a smaller tax called the mortgage stamp duty (around 0.4% of loan amount, capped at $500), which is usually included in legal fees. Also, HDB buyers have a mandatory fee for fire insurance (a small amount, under $10, at completion) and often pay for the valuation of the flat (~$120-$200). None of these individually break the bank like BSD, but they add up. The key is to have a detailed list of these government-related fees and make sure your cash/CPF savings cover them on top of the downpayment.

You’ll need a lawyer to handle the conveyancing (transfer of title, registering the mortgage, etc.). Legal fees for a typical property purchase can range from about $2,000 to $3,000 for HDB, and maybe $3,000 to $4,000 for private, depending on complexity and the law firm. If you’re taking a bank loan, sometimes the bank has a panel of lawyers and may even offer subsidies – e.g. some banks give a cash rebate or subsidy that covers legal fees partially or fully, as part of their home loan promotion. Keep an eye out for that when choosing a loan (Cashew’s platform highlights such perks in some bank packages). If you use your CPF for the purchase, there’s a small legal fee to withdraw CPF as well (usually included in the conveyancing process). For HDB loans, HDB charges some conveyancing fee too (which is usually lower than private lawyers). You generally pay part of the legal fee upfront (when work commences) and the rest at completion. It’s wise to budget at least $2,500-$3,000 for legal costs in your plan. Additionally, if you’re buying private property, you’ll want to do a home inspection or valuation – the valuation fee might be around a few hundred dollars (sometimes the bank’s valuation fee is separate). If you engaged a property agent to help you purchase a private property, the agent commission (usually ~1% of purchase price for buyer’s agent) is another cost; for HDB, buyer agents also often take a fee (up to 1%) but if you go through HDB resale without an agent, you save that cost. Negotiating these commissions is possible, but factor them in if you are definitely using an agent to represent you. All these transaction-related costs mean if you have, say, $50k saved exactly for a downpayment, you might actually need closer to $60k+ in hand to truly cover everything. Better to over-budget and be safe.

When you finally get your new place, will it be move-in ready? If you bought a brand new BTO, you’ll still likely need to do some renovation (flooring, built-in cabinets, etc., as new flats often come quite bare) and buy appliances/furniture. If it’s a resale flat or condo, you might want to renovate parts of it to your taste, or you may need to do repairs/replacements if the unit is aged (e.g. aircon, water heaters). Renovation costs in Singapore can vary wildly – from a modest $10,000 touch-up to $50,000 or more for a full makeover of a flat. First-timers often underestimate this. It’s important to decide early how you’ll budget for renovation. Some strategies:

Include renovation in your savings target: If you know you want a custom designed home, get quotes or at least ballpark figures (you can research or use renovation cost calculators online). Add that to your required savings so you don’t get a beautiful home but no money left to furnish it.

Stagger the non-essentials: Perhaps renovate the essential parts first (for example, the kitchen and bathrooms if they are unusable, or installing lights and basic built-ins). Other things like fancy feature walls or walk-in wardrobes can potentially wait a year or two until you save more, if budget is tight.

Use CPF for renovation? Unfortunately, CPF OA savings cannot be used for renovation or furniture – only for the property purchase and loan repayments. Some people take a renovation loan from a bank, but be cautious: those are unsecured loans with interest (typically ~3-5%) which adds to your debt load. It’s better to save up or use some cash on hand if possible, to avoid extra debt. If you must take a reno loan, keep it as small as possible and ensure the monthly payment plus your home loan still stays within a comfortable range.

Don’t forget furnishings and appliances: fridge, washing machine, maybe a new TV, bed, sofa – this could easily be another few thousand dollars even if you buy basics. You might space out these purchases or hold off on non-essentials (maybe your old furniture or hand-me-downs can last a bit). Many first-time homeowners also host housewarming parties – while that’s fun, the costs (and expectation to furnish nicely) can creep up on you! So plan for what you realistically need to spend in the first 3-6 months after getting the keys. Some try to include this in the renovation package; others allocate a separate sum.

Now that you’ll be a homeowner, there are recurring costs to prepare for. These aren’t exactly “hidden” since they happen after purchase, but you should account for them in your financial plan:

Monthly Maintenance or Conservancy Fees: If it’s a condo, the monthly maintenance can range from $200 to $500 depending on the property and unit size. HDB conservancy fees are much lower, typically under $100. These fees cover cleaning of common areas, security, etc. They will be a new bill to pay every month.

Property Tax: An annual tax on property ownership, which for owner-occupied homes isn’t too high for most flats (could be a few hundred dollars a year for an average HDB, more for high-end properties). Still, it’s a bill you’ll get from IRAS each year, so don’t be shocked by it.

Home Insurance: HDB requires a basic fire insurance (cheap). Beyond that, it’s wise to get a home content insurance policy that covers your renovations and belongings against fire, water damage, theft, etc. These policies might be $100-300 a year depending on coverage. It’s not mandatory (besides the fire part for HDB), but highly recommended to protect your investment.

Mortgage Insurance: Not required but often suggested – Mortgage Reducing Term Assurance (MRTA) or similar, which will pay off your loan if you pass away or become permanently disabled. If you have dependents (like a spouse or children who rely on you), this is something to consider. Premiums vary by age/coverage but plan for that if you take it up.

Utilities and Others: As a new homeowner, you’ll be paying for utilities (electricity, water, gas) directly – if you were living with family before, this might be new. Also, things like broadband, town council fees (for HDB), etc. should be in your monthly budget.

Finally, a smart move is to keep a reserve fund for your home. Life can throw curveballs – job changes, medical emergencies, or even something like a major repair needed (e.g. leaking ceiling, which if out of warranty might cost you to fix). Having 3-6 months’ worth of mortgage payments set aside as an emergency buffer is ideal. This could be part of your overall emergency fund, not necessarily separate, but earmark enough so that if anything happens, you won’t risk defaulting on your home loan or having to fire-sale the house. It provides great peace of mind.

By anticipating these hidden and ongoing costs, you ensure that the joy of owning your new home isn’t marred by financial stress. As the saying goes, plan for the worst, hope for the best – or in this case, plan for all the extra costs, and then enjoy your home knowing you’ve got them covered. If you need help figuring out these numbers, Cashew’s advisors can help you do a comprehensive affordability assessment (not just the loan, but total cost of ownership) so you’re fully prepared. With eyes wide open and budgets set, you can confidently take on the responsibility of your new home. Happy planning!

Whether you can afford a mortgage and whether you can manage it later in life are two sides of the same question. For upgraders, TDSR and age-related LTV rules shape what you can borrow, but the real risk lies in exit assumptions like sale timing and the HDB wait-out period. For retirees, refinancing with a new lender is difficult without income, but repricing with your existing bank typically does not require fresh income documentation, keeping your options open.

When upgrading from an HDB flat to private property, the key financing mechanics to understand are the 25% downpayment requirement (with at least 5% in cash paid at OTP exercise), and how CPF OA funds are disbursed. CPF OA is released directly to the seller at completion through your conveyancing lawyer, so you do not need to front that portion in cash and claim it back later. Upgraders should confirm TDSR headroom, map out their cash position at both OTP and completion, and instruct their lawyer on the CPF withdrawal early to avoid delays.

© 2026 Cashew. All rights reserved.