The first step is knowing your budget. Take a hard look at your finances to figure out how much home you can comfortably afford. In Singapore, this means considering your savings, CPF Ordinary Account balances, and monthly income. Remember that banks and HDB will use certain limits like the Total Debt Servicing Ratio (TDSR, currently 55% of your income) and Mortgage Servicing Ratio (MSR, 30% for HDB loans) to cap your loan amount. A quick way to gauge your price range is to use Cashew’s Mortgage Affordability Calculator, which factors in your income, debts, and current rules to estimate the maximum property price and loan you qualify for. By getting a clear budget up front, you can avoid falling in love with a home that’s out of reach and focus on options you can truly afford.

Next, decide what kind of property suits your needs and budget. In Singapore, first-time buyers often choose between an HDB flat (public housing) or a private property (e.g. condominium). HDB flats are generally more affordable and come with perks like government housing grants for eligible first-timers, but they have restrictions – for example, buyers must meet certain eligibility criteria (citizenship, household income) and adhere to a Minimum Occupation Period (usually 5 years before you can sell or rent out the whole flat). Private properties like condos offer facilities and potentially higher investment upside, but come with a higher price tag and no government subsidies. Weigh the pros and cons based on your lifestyle and finances. (If you need help, our AI Home Advisor can answer questions about HDB versus private housing.) By narrowing down the property type, you set a clear direction for your home search.

Sorting out your financing early will save you time and stress. If you plan to take an HDB loan for a BTO or resale flat, you’ll need to apply for an HDB Flat Eligibility (HFE) letter, which assesses your eligibility and indicates the maximum loan amount HDB can offer you. For a bank loan, it’s wise to obtain an Approval in Principle (AIP) from a bank, which is a conditional approval of the loan amount based on your financials. Getting pre-approved doesn’t lock you into a particular bank yet, but it gives you confidence on what you can borrow. The AIP (or HFE letter) typically lasts a few months, and having it in hand shows sellers you’re a serious buyer. Cashew can help you with this step by connecting you with the best bank loan options once you know your budget – our platform lets you compare rates across banks easily and even secure a pre-approval through our mortgage specialists.

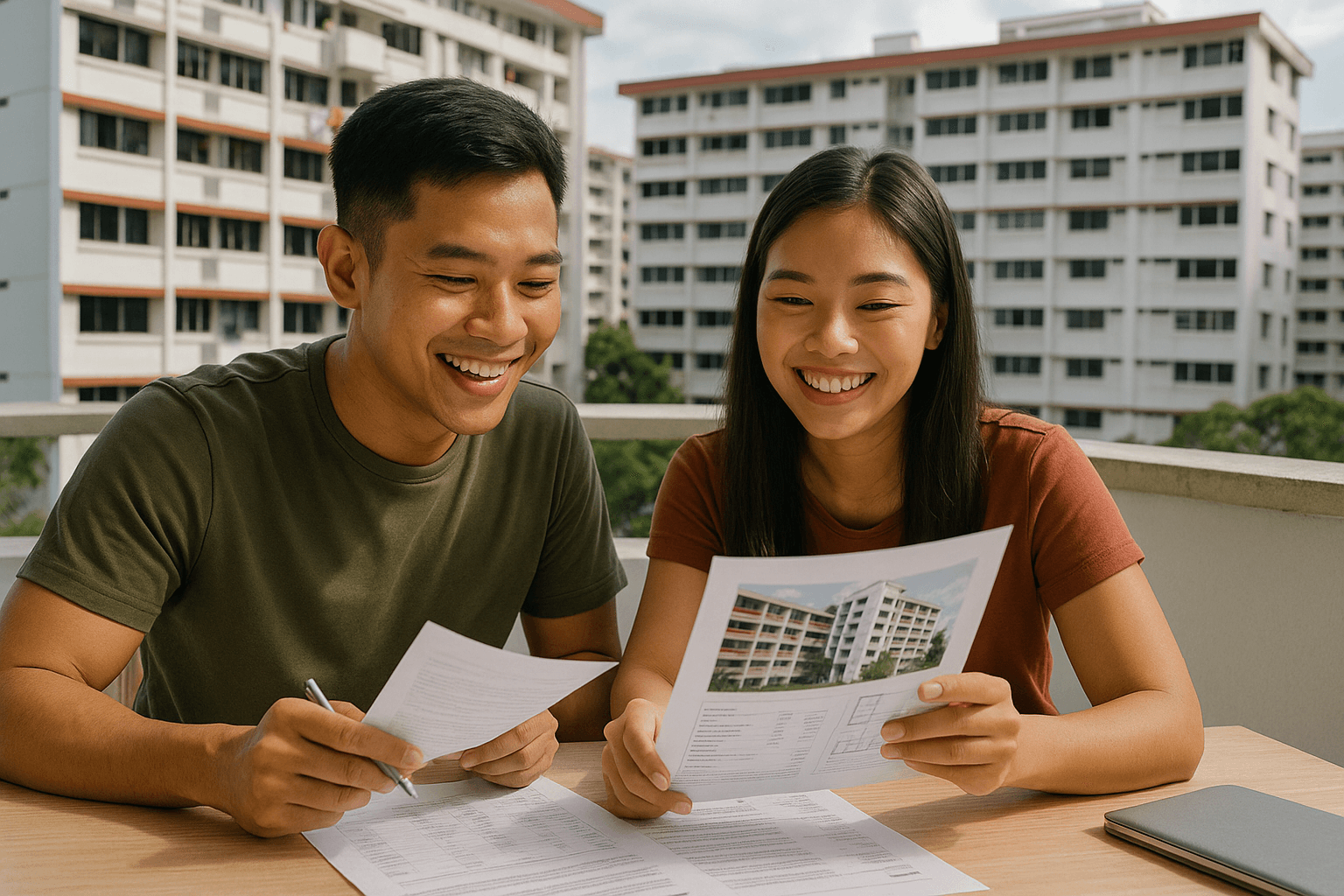

With budget and financing sorted, now comes the fun part: searching for your new home. Browse property listings on reliable portals, engage a property agent if desired, and visit showflats or open houses. Keep your budget discipline in mind – target neighborhoods and flat types or condo projects within your price range. For HDB BTO (Build-To-Order) flats, follow HDB’s sales launches and apply for the ballot. For resale HDB or private properties, attend viewings and ask questions about the unit’s condition, remaining lease (important for older HDB flats), and surrounding amenities. It may take weeks or months to find “the one”, so be patient. Make a checklist of your must-haves (e.g. proximity to MRT, number of rooms, high floor, etc.) versus nice-to-haves. This step can be time-consuming, but every viewing teaches you more about the market and your own preferences. Don’t hesitate to use Cashew’s resources or even ask our AI Assistant about neighborhood insights or property trends as you hunt.

Once you find the right home, it’s time to secure the property so no one else snatches it up. In Singapore, this is done by obtaining an Option to Purchase (OTP) from the seller. You’ll typically pay a small option fee as a deposit — for an HDB resale flat this can be up to $1,000, and for a private property it’s usually about 1% of the purchase price. The OTP is a legal document that gives you exclusive right to buy the property at the agreed price, for a fixed period (21 days for HDB, around 14 days for private property). Use this option period to finalise your decision and work out financing. Pro tip: Before putting down the option fee, ensure you’re committed, the price is right (you can check recent transaction prices in the area), and your loan pre-approval covers the amount. If everything looks good, go ahead and secure that OTP!

After securing the OTP, you’ll need to exercise it (for HDB, by signing and paying a further option exercise fee up to $5,000; for private, typically 4% of price to make total 5% deposit). This means you are officially going through with the purchase. Now the focus is on finalizing your home loan and legal paperwork. If you’re taking a bank loan, this is when you formally apply to the bank of your choice (you can use the bank from your AIP or choose another if there’s a better rate – Cashew’s mortgage brokers can help you quickly re-check which bank is offering the most competitive package for your situation). Submit the required documents (income statements, CPF statements, OTP details, etc.) to the bank for approval. Simultaneously, engage a lawyer for conveyancing: they’ll handle the legal transfer of property and coordinate between HDB or SLA (Singapore Land Authority) and the banks. You’ll sign the Sale & Purchase Agreement and mortgage documents, and pay the necessary fees like stamp duties (e.g. Buyer’s Stamp Duty, which is a percentage of the property price) at this stage. It’s a flurry of paperwork, but your agent, lawyer, and bank (or Cashew’s team if you’re using our service) will guide you through it.

Finally, the completion day arrives. For HDB, the completion appointment will be at HDB Hub; for private property, your lawyer will handle completion with the seller’s lawyer. The remaining purchase price is paid (with your CPF, cash, and loan funds disbursed by the bank or HDB), and you’ll receive the keys to your new home! Congratulations – you are now a homeowner. Before you pop the champagne, take note of a few post-purchase tasks: if renovations are needed, plan them before moving in; purchase fire insurance (mandatory for HDB loans) and consider home content insurance; set up utilities accounts; and update your address for billing. Owning a home is an ongoing responsibility, but you’ve made it through the buying journey. Whenever you need guidance – whether it’s about refinancing down the road or budgeting for renovations – remember that Cashew is here to help with tools and expert advice for every step of your home ownership journey.

Sales proceeds are what remains after deducting your outstanding home loan, CPF refunds (principal plus accrued interest back to your own account), and selling costs such as agent commission and legal fees from your selling price. The CPF refund is the most commonly overlooked deduction, as accrued interest grows over time and the amount returned goes to your CPF account rather than as cash in hand. Understanding these deductions in advance helps you accurately plan for your next property purchase or financial move.

Chiltern Park's two-bedders achieved a 43.92% average ROI over a decade due to four identifiable factors: a low entry price relative to fair value, location scarcity limiting new supply, a unit size with broad buyer appeal, and a modest quantum that supports liquidity. Buyers can apply this same framework to any project by assessing entry price against district comparables, surrounding land availability, unit size demand depth, and loan affordability across a full rate cycle.

© 2026 Cashew. All rights reserved.