Most homeowners can tell you exactly what they paid for their property. Far fewer can tell you what it is worth right now. That gap matters more than it looks, because almost every decision you make about your home is priced off today's value, not the figure on a purchase agreement you signed years ago.

That is the thinking behind our new home valuation tool. Enter your postal code and unit number, and in a few seconds you get an indicative value, the likely range around it, and a clear view of what that number unlocks. It is free, there is no sign-up, and we ask for no personal details to show you a result.

Your purchase price is history. Your current value is what banks, buyers, and your own next move actually respond to. Four examples make the point:

Refinancing: your loan-to-value, your eligibility, and the rates you qualify for are all calculated against what your property is worth today. A higher current value can move you into a lower LTV band and open up sharper pricing.

A new purchase: before you commit a single dollar, an independent estimate lets you sense-check an asking price against recent transactions rather than against the seller's optimism.

An equity term loan: the capital you can unlock is a function of current value minus your outstanding loan. If your property has appreciated, there may be more headroom than you think.

Selling: an independent reference point helps you anchor a realistic asking price, the kind buyers and their advisors will take seriously.

In each case, working from your original purchase price quietly leads you to the wrong answer. The valuation tool gives you the right starting number.

The flow is built to take seconds, not appointments:

Enter your details: pop in your postal code and unit number. If you want a sharper estimate, you can add your floor area.

We value your unit instantly: we autofill your address and run an indicative valuation against recent transactions.

See what it unlocks: alongside your value, you get the likely range, your indicative loan-to-value, and the moves your number makes possible.

No paperwork, no waiting, and no obligation to do anything afterwards.

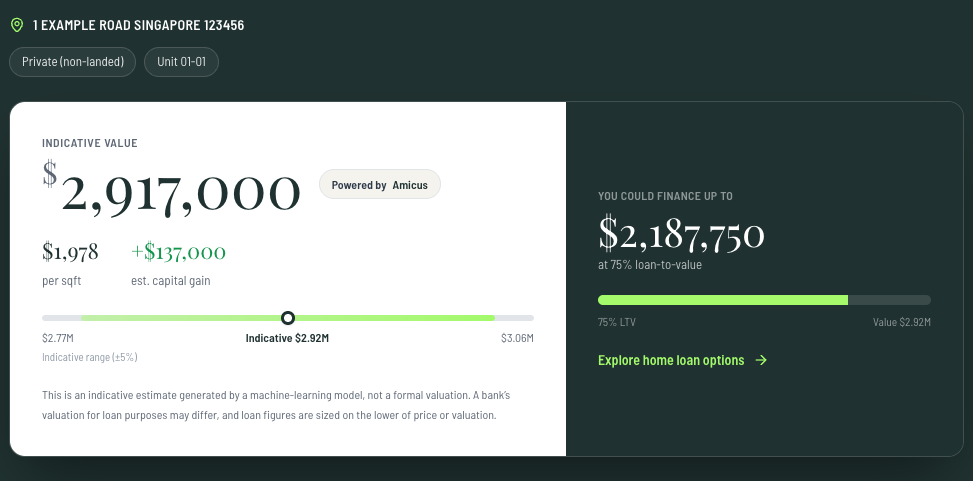

An indicative home valuation in seconds.

An indicative home valuation in seconds.

The estimate is produced by Amicus, a Singapore data company that has been operating since 1985, using the same automated valuation approach that banks rely on rather than a number we set ourselves. The model draws on close to three decades of Singapore transaction data and factors in location, floor level, built-in area, and recent comparable transactions. For HDB flats, it also accounts for flat type, model, remaining lease, and the HDB Resale Price Index.

It is an Automated Valuation Machine, the same class of model used across the industry to value property, and it is built by a team with deep roots in Singapore proptech. The result is a figure grounded in real market data, not a guess.

Being precise about the limits is part of being useful. The valuation is an indicative, machine-generated estimate, not a formal valuation, and it deliberately leaves a few things out:

Cash over valuation: any premium a buyer might pay above the valuation is not reflected.

The condition of your specific unit: renovations, wear, and the particular state of your home are not assessed.

A bank's own assessment: when you borrow, the bank runs its own valuation and sizes the loan on the lower of price or valuation, which may differ from this estimate.

Think of the number as a well-informed starting point that tells you where you stand, not a substitute for a formal valuation when one is required.

A valuation is only useful if it leads somewhere. So the results page does more than show a figure. It connects your value to the decisions that follow:

Relevant loan packages: the best rate in each category, sized to your indicative loan, drawn from live data and updated as rates move. Cashew works in partnership with all major banks and lenders, so you are seeing the market, not a shortlist.

A mortgage calculator: pre-filled with your indicative loan and the best matched rate, so you can adjust tenure and rate and watch your monthly repayment update.

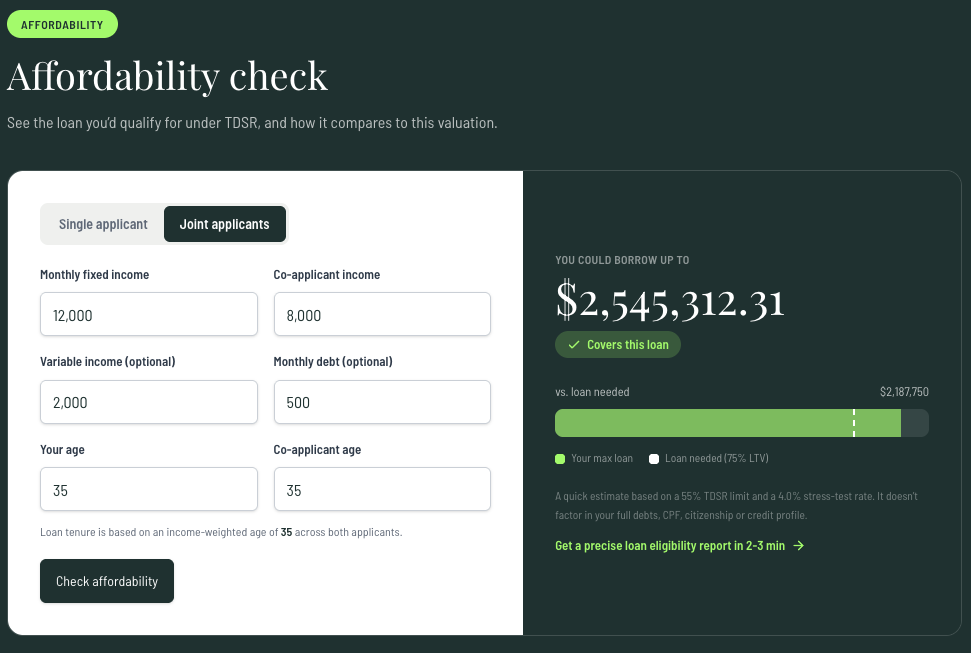

An affordability check: enter your income and see the loan you would qualify for under TDSR, measured against this valuation.

Example affordability calculation based on home valuation.

Example affordability calculation based on home valuation.

When you are ready to go further, you can speak to a Cashew advisor for tailored guidance on a purchase, a refinance, or unlocking equity. Free, and with no obligation.

Knowing what your home is worth should not require an appointment, a sign-up form, or a sales call. Pop in your postal code and see your number in seconds.

© 2026 Cashew. All rights reserved.