What Is a Mortgage Factsheet?

When you click on a mortgage package on ACCESS by Cashew, you'll be able to download a standardised one-page factsheet that summarises every critical detail of the loan -- the rates, penalties, lock-in terms, rebates, and fine print -- all in the same layout, regardless of the bank.

The format is always the same, so once you learn to read one, you can read them all. To walk you through it, we'll use a real example: the UOB Fixed 3-Year package for HDB flats. But everything below applies to every factsheet you'll see on ACCESS -- whether it's DBS, OCBC, Standard Chartered, or any other bank.

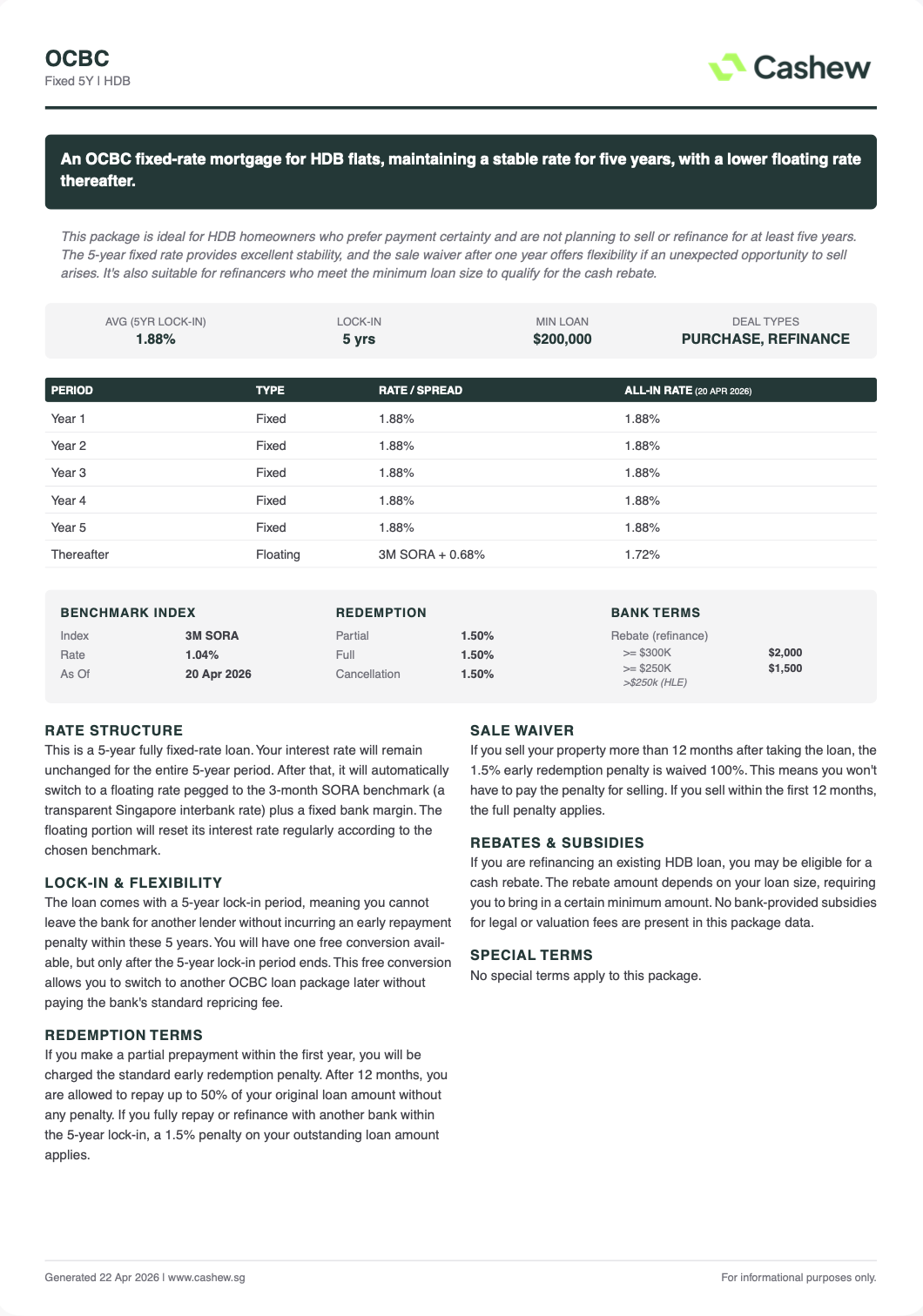

Image 1: UOB 3 Year Fixed Factsheet

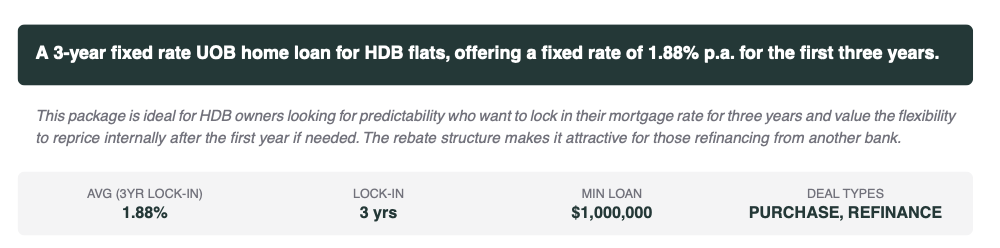

1. The Header

Every factsheet begins with a headline that describes the package at a glance, followed by a brief summary that explains who this package is most suitable for. Then come 4 key stats:

- AVG RATE (LOCK-IN PERIOD): The blended average rate across the lock-in period. Use this to quickly compare packages with different step-up structures.

- LOCK-IN PERIOD: How long you're committed to the bank. Leaving before this ends triggers an early redemption penalty.

- MINIMUM LOAN: The smallest loan size that qualifies for this package. Varies widely between banks and packages.

- DEAL TYPES: Whether the package is available for new purchases, refinancing, or both.

Image 2: Example: UOB 3 Year Fixed Header Table

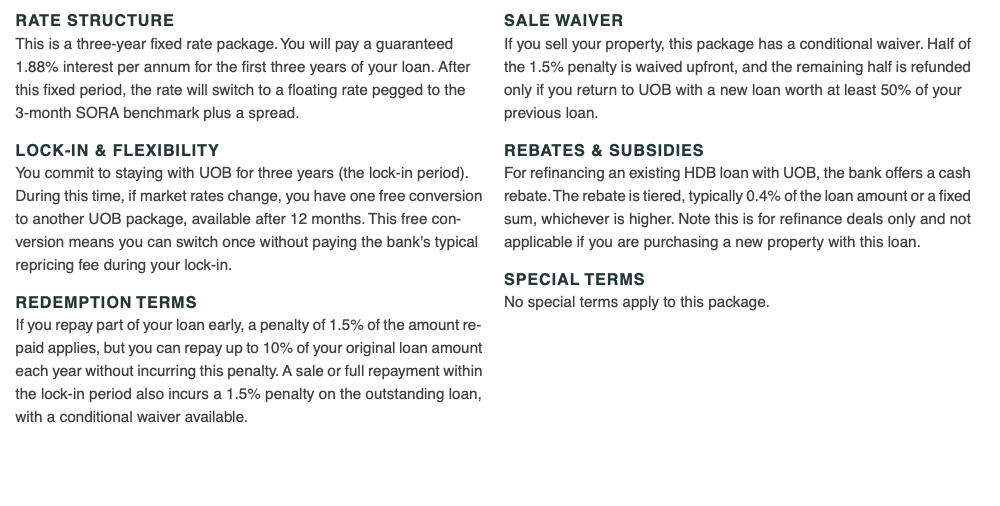

2. The Rate Table

The rate table shows the interest rate for each year of the loan, broken into four columns: the period, the type (fixed or floating), the rate or spread, and the all-in rates of a specific date.

Here's how to read each column:

- PERIOD: Each row is one year of the loan. The final row, "Thereafter," is the rate that applies for the rest of the loan term once the fixed or step-up schedule ends.

- TYPE: Tells you whether that year's rate is fixed (locked in, won't change) or floating (moves with a benchmark like SORA). Some packages are fully fixed, some fully floating, and some are a mix -- fixed for the first few years, then floating.

- RATE / SPREAD: For fixed-rate years, this is simply the interest rate. For floating-rate years, this shows the bank's margin (the "spread") on top of a benchmark index. In our UOB example, the "Thereafter" row shows "3M SORA + 1.00%" -- meaning UOB adds a 1.00% margin to whatever the 3-Month SORA rate is at that time.

- ALL-IN RATE: This is what the client actually pays today. For fixed years, it equals the rate itself. For floating years, it's the benchmark rate + the spread, calculated as of the date shown on the factsheet. Since SORA moves, floating all-in rates are a snapshot, not a guarantee.

Image 3: UOB 3 Year Fixed Rate Table

3. The Benchmark Index, Redemption and Bank Terms

The Benchmark Index anchors all floating-rate calculations on the factsheet. It's your go-to when a client asks "what rate am I getting?" For packages with a fixed period, like this UOB one, the benchmark only kicks in after the fixed period ends -- but it still shows what the post-lock-in rate would look like today.

The Redemption section shows the cost of exiting the loan early, broken into three figures: Partial Redemption (paying down more than your annual free allowance, typically 10%--50% of the original loan), Full Redemption (paying off the loan or refinancing with another bank before the lock-in ends), and Cancellation (withdrawing after accepting the Letter of Offer but before drawdown).

The Bank Terms section covers cash incentives, mainly refinance rebates tiered by loan size. Here, UOB offers 0.4% of the loan amount for loans of $100K or more, or a flat $2,000 for loans above $250K -- whichever is higher. Rebates vary across banks and packages, and most only apply to refinancing, not purchases.

Image 4: UOB 3 Year Fixed Benchmark Index, Redemption and Bank Terms

4. The Details

Every factsheet includes a set of plain-English summary cards covering the key terms. These are your quick-reference panels -- each one distils a complex clause into a sentence or two. Here's what you'll typically find:

- RATE STRUCTURE: Explains whether it's fixed, floating, or a hybrid -- and how the rate changes over time. For our UOB example: fixed at 1.88% for 3 years, then floating at 3M SORA + 1.00%.

- LOCK-IN & FLEXIBILITY: The lock-in duration and what happens during or after it. This UOB package offers one free conversion to another UOB package after just 12 months -- even though the lock-in is 3 years. That's a notable flexibility perk.

- REDEMPTION TERMS: The penalty-free repayment cap and when it applies. Here it's 10% of the original loan per year -- one of the tighter caps you'll see. Beyond that, the 1.5% penalty kicks in.

- SALE WAIVER: What happens to the penalty if the client sells. UOB offers a conditional waiver: 50% waived upfront, and the other 50% refunded only if the client returns with a new UOB loan worth at least 50% of the previous one.

- BANK TERMS: Cash rebate details for refinancing customers, restated in plain English.

- SPECIAL TERMS: Anything unique to this package -- such as a choice of SORA benchmark, subsidies for legal fees, or other perks. If nothing applies, this card will say "no special terms," as it does here.

Image 5: UOB 3 Year Fixed -- Rate Structure, Lock-In & Flexibility, Redemption Terms, Sale Waiver, Rebates and Subsidies & Special Terms

5. Your 5-Point Checklist

No matter which factsheet you're looking at, here are the five things to check:

- AVERAGE RATE: Your quick comparison number. Fixed averages are guaranteed; floating averages are snapshots.

- LOCK-IN: How long the client is committed. Longer lock-ins mean more certainty but less flexibility.

- REDEMPTION TERMS: The penalty percentage and the annual penalty-free repayment limit. Check when the free cap starts and how generous it is.

- CASH REBATES: Does the client's transaction type (purchase vs refinance) qualify? What's the minimum loan to unlock it?

- SALE WAIVERS: If the client might sell during the lock-in, how much of the penalty is waived -- and are there conditions like re-borrowing?