For nearly two years, Singapore homeowners on floating-rate loans have ridden a steady tailwind: falling interest rates. Every reset brought a slightly smaller repayment. That chapter now looks like it is closing.

In May 2026, 3M-SORA, the benchmark behind most floating-rate home loans in Singapore, edged up for the first time in two years. It is a small move, but the direction matters.

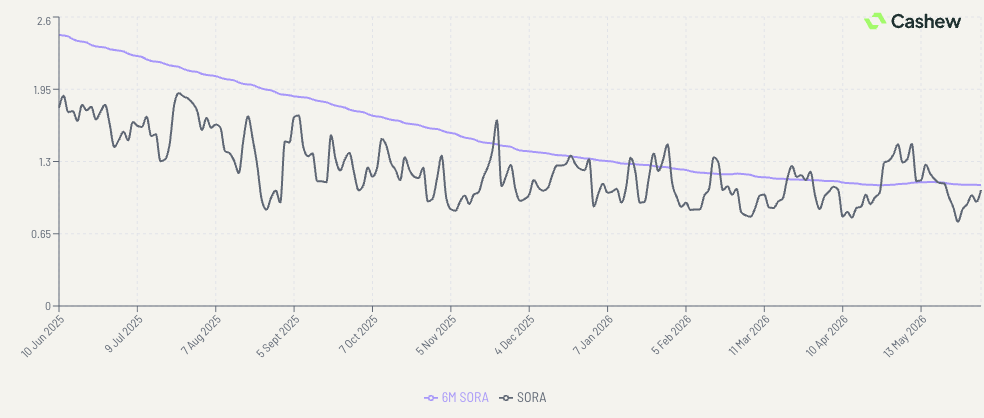

A few numbers tell the story:

In plain terms: the rapid drop in home loan rates that many borrowers enjoyed appears to be bottoming out.

SORA and 3M Compounded SORA over the last 12 months

SORA and 3M Compounded SORA over the last 12 months

Two forces are pulling in the same direction:

The US Fed is staying higher for longer: Markets are now pricing in zero US rate cuts for 2026. Singapore rates tend to track US rates closely, so when the Fed holds, our rates have less room to fall.

MAS tightened in April: The Monetary Authority of Singapore firmed up its policy stance in mid-April, which has supported domestic liquidity conditions. As the gap between Singapore and US rates narrows, SORA naturally edges higher.

It is worth keeping perspective on the wider backdrop. Oil retreated roughly 20% from its 2026 peak in late May on optimism around a US-Iran ceasefire, which eases imported inflation pressure. That conflict is still unresolved and markets remain volatile, so the outlook can shift. The base case from the research, though, is stabilisation rather than a return to aggressive hikes.

The right move depends entirely on your situation, but here is the lay of the land:

If you are on a floating, SORA-pegged loan: The run of steadily shrinking repayments is likely ending. Your monthly instalments may flatten out, and could tick up modestly over the rest of the year. This is not a reason to panic, but it is a reason to check where your package sits.

If you have been weighing fixed versus floating: When rates were clearly falling, staying floating made sense, because you captured each drop. With rates now stabilising and carrying a mild upward bias, that trade-off is more balanced. The premium you pay for the certainty of a fixed rate looks more reasonable than it did a year ago.

If your lock-in is ending soon, or you are sitting on an older high rate: This is a good moment to review repricing or refinancing while pricing across lenders is still competitive. Acting before rates drift higher tends to be easier than reacting after.

One quieter tailwind for borrowers: banks' funding costs have stayed stable, which helps keep home loan pricing competitive for now. That window may not stay open indefinitely if rates continue to firm.

There is no one-size-fits-all answer here. The right call depends on your loan type, your remaining lock-in period, how long you have left on your tenure, and your plans for the property. A borrower two years into a low fixed rate is in a very different position from someone whose floating package resets next month.

This is exactly the kind of decision worth running past someone who can look at your specific numbers. At Cashew, our advisors work in partnership with all major banks and lenders, so we can compare your current package against what is available across the market and tell you whether repricing, refinancing, or simply holding makes the most sense for you.

If your home loan is up for review in the next few months, now is a sensible time to take a look. You can also keep an eye on where rates are heading on our daily updated SORA tracker.

This article is for general information only and does not constitute financial advice. Interest rate figures reflect the latest available data as of May 2026 and are subject to change. For guidance on your specific situation, speak to a Cashew advisor.

© 2026 Cashew. All rights reserved.